The blog is written by Amit Agrawal. The Author is a MBA student of IFMR GSB at Krea University

If you think economic super-powered China as the fastest growing economies in the world due to its 6-7% consistent growth rate, probably you might want to twitch your nerves again. China is not even in the top 20 fastest growing economies on the planet. In fact, about 38% of the top 50 fastest growing economies comes from one single continent.

‘Afri-terra’ (later Africa).

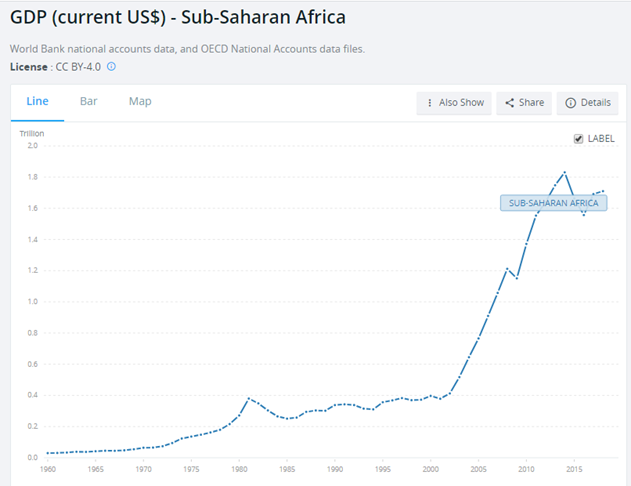

A leap in 2002 says that the GDP per capita of Sub-Saharan Africa was a paltry $588b. Yet by 2019, the GDP per capita had grown to well over $1600b – A 172% spurt increase in the wealth of the continent in less than two decades. This massive increase in wealth has brought Nigeria, Botswana, and Ghana out of relative poverty.

But what has brought Africa’s economy out of poverty? Or more importantly, who has brought it out?

Africa has been the most underdeveloped continent over the last several centuries; it has only 60,000 km of highways constructed in the entire 30.4 million km2 surface area, while the US stands with 108,000 km of highways in a 9.8 million km2 area. In fact, to this day there are still no paved highways that travel through anywhere in Central Africa. And the transportation network has been just one of a litany of infrastructure flaws in Africa. It had problems with electricity availability, internet access, and water shortages as well.

But things started to change just a few decades ago.

China slowly started gaining large amounts of influence in Africa post 1970s. It did this by increasing foreign aid and trade with many African countries and investing billions per year in African infrastructure projects. For example, Africa’s main railways in Kenya, Ethiopia, Angola, Djibouti, and Nigeria are all funded by China. They also funded for major Headquarters, Zimbabwe’s new parliament building, several major power plants, oil refineries, and an entire city in Egypt.

But why is China investing so much money in Africa?

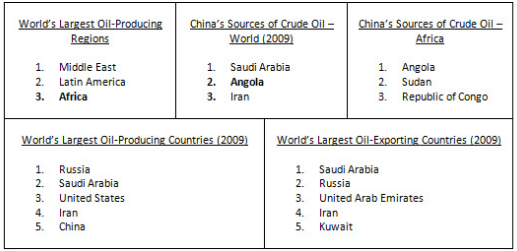

Reason? ‘Resources’. China trades for one-third of crude oil against $128b with Africa.

Political Influence. At any of the UN special session votes: from voting on the status of Jerusalem to voting on human rights violations in Myanmar, Ukraine, Iran, and Syria, a large portion of African continent did not go against China. Now, my say isn’t that China is buying votes at the UN but at the very least China has probably influenced the voting pattern of many African nations. The same could very well be said for the US influence on many Western countries.

Labor. China began shifting a lot of its labor industries to Ethiopia due to cheaper labor. It is estimated that roughly 12% of Africa’s manufacturing production today is being run by Chinese companies.

ROI. China has pumped in money into Africa for good returns. From 2006 to 2011, the average return on African investments for China was a hefty 11% per year. In fact, roughly 15% of all African debt is owned by the Chinese government, and two-thirds of all loans given to African nations in the past 3 years have come from China. In 2018, China announced of financing $60b solely for Africa over the next decade.

Amidst this Chinese heavy investments, big tech is contributing to Africa’s modernization for last ten years. The South Korean company, Samsung, viewed Africa as the next giant consumer market and doubled its investment (2012) to become the most valuable phone company on the continent. But recently the true winner of this race was Huawei. As part of China’s plan to build up the infrastructure of Africa, they also ended up building over 70% of Africa’s 4G and 5G networks – meaning that at the end of the day, Huawei may not be the king of the smartphone market but they are the undisputed champion of the telecom industry.

Amazon’s $100m data-centre in Cape Town, Facebook’s multi-billion dollar ‘Project Simba’ and Google’s Equiano marks the booming African investment. Other notable investors are Microsoft, Netflix, IBM, Cisco, and Uber.

Overall, an influx of investments from both American and Chinese companies coupled with an increase of trade and investments from some national governments created an economic battleground. Companies and governments can build up Africa’s infrastructure the fastest, and dominate the emerging markets before its competitors can which resulted in some rapid modernization in infrastructure. For example, as compared to 2000, today roughly 45% of the population has access to electricity against 26% and 40% of the continent now has access to the Internet against 1%.

The biggest factor for Africa’s future economy might be Africa itself. Take for example, ‘Jumia’ – launched as an African e-commerce startup, expanded, got listed, and valued at a billion dollars. McKinsey’s database of large businesses in Africa reveals 400 companies earns revenue of $1b or more and nearly 700 companies have revenue greater than $500m. Another positive sign was when Africa witnessed the African Continental free-trade agreement (March 2018) for the purpose of making Africa a single market thereby deepening the economic integration of the entire continent. Projections state that this trade agreement could lift intra-African trade by up to 52%. But this is just one step.

BOTTOM LINE

Africa has been popularly called as ‘Sleeping Giant’ and now with the rise of globalization, it is reaping the fruits of it. Countries like Rwanda have defied the odds predicted by Western countries. People should stop looking Africa as the world’s charity bowl and rather start investing in it. India, being the forerunner, plays a key role in building up African economy particularly in nations like Kenya, Nigeria, South Africa, Mozambique, and Mauritius. Given the pandemic-negative news hovering over Africa, they need to do a lot more to be considered as the modernized economy.

The opinions expressed in this article are those of the author. They do not reflect the opinions or views of Krea University or its members.

The blog is written by Aviral Singh. The Author is a MBA student of IFMR GSB at Krea University

Businesses across India have come to a grinding halt as they fight a prolonged war against Covid-19. This disruption has caused serious cashflow problems for various firms across sectors. At the forefront of this backlash are Non-Banking Financial Companies. After the fall of IL&FS, the lenders have been wary of lending money to them and with lockdown in place, it is bound to hit their customers who mainly belong from semi-formal sectors of infrastructure industry as the demand for property goes down. Adding fuel to the fire was the decision of RBI last month which obliged them to give moratorium of three months to their borrowers citing the reason that many of them belong to that part of the economy which will be worst hit due to this pandemic however it left the banks (Major source of funding for NBFCs) with the choice to decide on their discretion to pass on the benefit of the moratorium to NBFCs and given the poor credit history of the majority of them most of the banks were reluctant to pass the benefit of the moratorium to these companies. That came as a double whammy for cash strapped companies, on the one hand, it has blocked their source of income as people will avoid paying their debts back due to the seizure of business activities as well as uncertainties in the future business scenario and on the other hand it has forced them to pay their debts and bond payments despite their poor financials, hence taking away more liquidity.

What if these NBFCs delay their bond payment for this period and payback later?

There’s a clearly defined rule in bond markets which obliges the issuer of the bond to make the required repayment on the date at which their bond matures and if they fail to do so the bond is put under the category of default which can lead the company to get a credit rating of “D” hence closing all gates for it to borrow in the future. So that is a complete NO for a company given the current liquidity crisis.

RBI decided to lend the banks Rs 1 Lakh crore in four equal tranches (25000 crores) starting from March 27 till April 17 2020. Under this, if the bank bids for any amount it was eligible to get it at the current repo rate (Subject to change as per changes in repo rate in future) for a period of 3 years. After securing the amount the bank was to purchase fresh bonds of NBFCs, Corporates & PSUs in next 30 days and if it fails to do so they were to pay 2% higher interest. In order to ensure that the banks purchase bonds from as many entities as possible, they were restricted to buy not more than 10 % of the allocated amount from a single entity. They were also directed to use only 50% of their allocated fund for new issues whereas the rest should be used for purchase from secondary markets. The banks were given the facility of no intermediate repayments but were supposed to pay back the money taken from RBI at maturity along with the interest.

This opened the way for injection of liquidity for NBFCs as now they can issue new bonds which had a buyer and given that the banks borrowed the money from RBI at the current rate of 4.4% the banks had an opportunity to purchase bonds which gave them the opportunity to earn 6-7% of interest on the amount invested in non banking financial companies if held till maturity the deal looked enticing but as the credit risk associated with NBFCs were huge most of the money by banks were deployed to financially stable large corporations and public sector undertakings leaving the crisis of non-banking sector companies unattended.

RBI brings TLTRO 2.0, Says NBFC only!!

This time the RBI wanted to make sure that the benefits of TLTRO allocations should reach NBFCs so it put forward the condition that the money cannot be allocated in buying corporate bonds and banks can only purchase NBFCs bonds and it introduced more categories and conditions this time to make sure that NBFCs of all size got the intended liquidity push.

RBI decided to allocate Rs 50000 crore under TLTRO 2.0 which will be given in two equal tranches with the initial bid on 23rd April 2020. This time the banks were directed to follow some additional condition in deploying this capital. 10% of the issued fund will be earmarked for Microfinanciers, 15% of the issued fund should be used to purchase the bonds of NBFCs with assets worth of Rs 500 crore or below, 25% of the allocated money should be used to purchase bonds of NBFCs with asset size of Rs 500 Cr- 5000 Cr and the remaining 50% were at the discretion of Bank to be allocated as and how they would choose to. The banks were now free to purchase as much as they want from any company and any market (Primary or Secondary) and also the minimum time given to allocating the funds was increased from 30 to 45 days.

How’s the josh shown by banks?

Unlike expected by RBI, It instead got a cold shoulder from banks as only 14 bids worth Rs 12,850 crore came in as against Rs 25000 crore which was up for offer which was way less than the 18 bids of Rs 1.14 trillion which were received on April 9 during the TLTRO 1.0 (Remember in TLTRO 1.0 banks were allowed to deploy the allocated fund to purchase bonds of corporates and PSUs) clearly showing that even the relaxation in certain criteria wasn’t able to push banks in buying NBFC bonds due to the threat of credit risk despite for a great opportunity to earn higher returns. The banks wanted to play safe.

What did the Bankers argue to support their behaviour?

The bankers have been complaining that it isn’t an easy job to find investment-grade papers of these lower varieties and given the risk of being penalized if they are unable to allocate the money after borrowing from the bank as they are unsure of the timely returns, they avoided bidding for TLTRO. The situation would have been different for them if there has been no categorization by RBI in allocating the funds which currently mandates them to allocate a certain percentage in low rates papers. (However, if not for these rules the whole purpose of liquidity injection in small and severely hit NBFCs would have been defeated). Too much of subdivision has scared away the bankers. They have suggested that instead of being asked to just purchase bonds which is time-consuming they could also be allowed to give loans to NBFCs & MFIs. Some also suggest that TLTRO 2.0 should be priced at 3.75% which is the new overnight rate giving them an opportunity to make good profit from financially better-positioned companies hence helping them to hedge the risk of losing money by investing in weaker ones.

The road ahead for NBFCs

Approximately Rs. 63000 crore worth of commercial papers and non-convertible debentures is going to mature for big NBFCs in the course of next six months which means even if banks will buy Rs 25000 crore worth of bond it would only suffice for half of their money requirements the other half has to be brought in through other routes like bank loans, the recollection of loans and selling its bonds to retail investors and mutual funds which in the given scenario is easier said than done. Which in a nutshell has been successful in sending cold shivers to the companies in this sector and has sent RBI back to contemplation mode for planning another way to provide liquidity push to this sector

What do the experts and industry veterans have to say?

From what I was able to read, hear and extract out of many experts through news and social media is that given the scenario if RBI really needs to make a ground impact on this one than it could look west for guidance (US Fed). In the United States, the Federal Reserve Bank directly buys commercial papers unlike RBI which use a pass-through vehicle like TLTRO which help it in keeping the credit risk at bay (Risk hedged to Bank)

That RBI should open a direct window for NBFCs and Mutual Funds ( I know Franklin Debt Fund Fiasco came to your mind) instead of offering liquidity through banks, Yes I sense you this sounds a radical measure and needs much deliberation to think about its practical viability but given that lately, we have banks shying away even from some of the financially sound NBFCs (Many of them with capital adequacy ratio of 18% or above) it is high time that RBI must lead from the front to rescue this cash-starved sector and I close as I quote the words of Finshots ( Providing finest financial insights daily) here in the context of the central bank of India in this hour of crisis “Maybe, just maybe, what this country needs is a Dark Knight, a silent guardian, a watchful protector”

The opinions expressed in this article are those of the author. They do not reflect the opinions or views of Krea University or its members.

The blog is written by Aviral Singh. The Author is a MBA student of IFMR GSB at Krea University

India is the third-biggest oil consumer in the world after The United States & China. It imports approximately 82% of its oil needs. Due to its heavy dependence on foreign markets for oil, it cost a lot on the country’s financials. India spent US$ 63.305 billion in the financial year 2017-18 on its crude oil imports. Moreover, it’s high reliance on foreign nations for its oil needs forces India to formulate its foreign policy accordingly and always possess a strategic challenge for India to meet its demand should there be any unforeseeable event.

In order to mitigate that risk, India came up with underground strategic oil reserve facilities at Vishakhapatnam, Mangalore and Padur. Which has a combined storage capacity of 5.33 million tonnes. Once full these reserves can help India meet 9.5 days of its oil needs. Given the rising demand for energy needs in India and oil forming a large proportion of it the government value these reserves a lot and always hunt for getting a good bargain in terms of price for filling up these reserves.

In the present scenario, the price of Brent crude is tanking like never before. While you think that it is all because of the slump in global oil demand due to Covid-19 outbreak you are seeing only half aside of the coin. Oil prices can be kept at high-profit margins despite demand slump if the supply is controlled through production cuts. OPEC along with Russia and The US are 3 big stakeholders when it comes to oil supplies. All 14 nations of OPEC wanted to cut the production so as to keep the prices of oil steady but non-compliance with Russia which is the third-biggest oil supplier has led them into a production war with both parties keeping the supply steady and even ramping up at times which combined with the huge drop in demand due to covid-19 outbreak it has lead to the sharp decline of oil prices a 40% drop in its price in March and right now the price of it is trading between $ 20- $ 30 per barrel which is at a record low.

This has led to the huge opportunity for high consuming high dependent oil importer India which can take advantage of low oil prices. However, sluggish growth of the economy due to low demand and the covid-19 outbreak has come as a double whammy for India which has resulted in low demand for oil from in the past few months. It can be observed from the fact that the demand for diesel which accounts for about 40% of the country’s oil requirement fell 7.4% in October 2019 due to slow growth in the economy. With that being said it happens to be that India has found another way to turn this tide in its favour despite all the odds and that is by ordering middle eastern oil to fill up its reserves. This single move has led to the serving of two important purposes which are of long-term importance to India both in terms of trade and diplomacy. First to take advantage of low oil prices to fill up its 5.33 million tonnes of empty oil reserves which are created by India Strategy Petroleum Reserve Ltd and it is being done by buying Brent crude worth of Rs 5000 crore at the dirt-cheap rate of around $ 30/barrel and secondly by giving a strong signal of solidarity to its trade partners and strategic allies in The OPEC and USA by doing its bit to stabilize the plummeting oil prices and help bridge the demand-supply gap.

I believe such a strategic move in this testing times is a masterstroke in the favour of nation from every aspect and has already started paying dividends by helping us to fully load our strategic reserves without a heavy hole on our critical current account deficit. On the diplomatic front, such gesture by India will be seen as a friendly move towards our high-value partners in the middle east which play a crucial role in both shaping up the national security policies and deciding the efficacy of foreign policy.

A lot of managerial learning to take away here especially with respect to long term vision and strategic thinking while decision making which was portrayed by our bureaucrats in this low profile yet crucial decision which was taken recently.

The opinions expressed in this article are those of the author. They do not reflect the opinions or views of Krea University or its members.

The blog is written by Rajashree Sadhu. The Author is a MBA student of IFMR GSB at Krea University

“God always have a better plan for us, though the process might be hard and painful!” that’s what my grandfather told me always. Hey wait, I am not writing this article to give you philosophical advices.

But………. Then What?

Well, this abrupt lockdown of the entire world has bought a lot of unexpected dismay in our lives (especially migrant’s workers and not so privileged section of the society). Yet, isn’t that’s what life is, it happens to us when we are busy having other plans.

We are continuously worried and grumbling about negative things that we are facing due to this pandemic- loss of lives(due to Covid-19), job losses, salary cuts, internships cancelled, business at halt, economy is at a standstill, disruption in supply-chain and above all ‘THE GREAT RECCESSION’ (on its way).

But salute to the frontline warriors- doctors, nurses, policemen, sanitation workers and others who are working day in and day out to help us overcome this tough situation. This pandemic coupled with lockdown (which is the only solution to stay safe) has put humanity into a huge test. It’s an opportunity for all of us to serve the under-privileged section of the society who are not able to get their daily bread due to lockdown and no earnings.

Yet some miserable incidents are happening in few places – like pelting of stones at policemen, doctors when they are trying to help us in this pandemic, such incidents are really unforgiving. This is not the time when we should believe in rumors, be arrogant and thereby create violence in society. We all have to fight this together and cooperate with the frontline workers.

This time too shall pass, so we should focus on the positive things that we are experiencing and how can we make the most of the time that is available to us. If you ever felt that you lack time to do the things you wanted to do then this the opportunity. Up-skilling ourselves, improving our fitness, spending time with family these are the things we always wanted to do. Life always comes to us with surprise gifts, blessings and of course hurdles which makes our lives even better.

We neither know how long will this pandemic last nor how long will this lockdown continue, but we can hope that this period will be over really soon. Optimist will always love to see the positive side of things and so if we look deeper we will realize the good things that we are experiencing at this point.

The environmental pollution levels have gone down drastically, rivers are cleaner than we have ever seen before, we are able to breathe fresh air again and a few endangered species have started to appear in few places. This makes us realize that apart from human beings other animals too have equal rights to live in this planet. Nature always has its own healing process but in our rat race to achieve more we forget that, what we are experiencing now is nothing but the collective karma to humankind! Mother Earth will come alive again and it will be more vibrant than ever before.

There is another aspect of this pandemic- a lot of business opportunities will come up. Make in India and manufacturing sectors will be boosted up far more. Every country from now on will try to be self-reliant. The change in consumer behavior will open up new avenues for businesses. Fintech, digital payments, e-commerce will experience a big boom in the days to come. Medical infrastructure will gain more importance than ever before.

Most importantly this lockdown has provided us a huge lesson- no work is small, everyone has its own importance starting from a rag-picker to a top notch celebrity. Today, we should all be grateful to the doctors, paramedical staffs and nurses who are saving millions of lives in this pandemic.

Life always allows some crisis to occur, before revealing its full bright side. As every cloud has silver lining so does everything in life, for a period we are having a tough time but we will be victorious one day. This crisis will give us the zeal to put the best in whatever we do as don’t know when our day is. This Corona Virus will take away a lot of things from us, but in return it will provide us a life time lesson that will help us in the long run.

The blog is written by Jaykumar Patel. The Author is a MBA student of IFMR GSB at Krea University.

A Cryptocurrency is a digital currency that is created and managed through the use of advanced encryption techniques known as cryptography. Cryptocurrency leaped from being an academic concept to (virtual) reality with the creation of Bitcoin in 2009 by the launch of “White Paper” by “Satoshi Nakamoto”. Bitcoin which I guess most of the people know for its significant growth in a short period of time, be its surge in price by 10 times as it peaked its value in April, 2013 in just two months from a mere low of $266 per Bitcoin. Or the Bitcoin during the most amazing period of Bitcoin bubble in 2017 which ultimately crashed in the beginning of 2018. But somehow cryptocurrencies still stand out to be different from the normal Fiat money.

Why Cryptocurrency?

Cryptocurrency is a virtual currency which is decentralized in nature that uses peer-to-peer technology. It enables all the functions such as currency issuance, transaction processing and verification. The real secret technology backing the cryptocurrency is the Blockchain Technology, which in expert’s view can be named as the technology which is going to change the world. Just like what the internet did to the world starting from the early 1990s, what Mobile connectivity did to the communication (telecommunication) industry from the early 2000 till now. Blockchain is going to play the same role for the world in the coming years as backed by many researchers. Blockchain technology is most simply defined as a decentralized, distributed ledger that records the provenance of a digital asset. The same system and technology which ensures the security of the cryptocurrency.

To make the understanding simple, here we will just consider the most well-known cryptocurrency i.e. Bitcoin.

Bitcoin vs Fiat money

Bitcoin is a decentralized, not governed by a central authority. But is generated by the miners which are spread all across the globe and hence is manipulation free or free from any government interference. The value of a Bitcoin is wholly dependent on what investors are willing to pay for it at a point in time. The security and credibility of bitcoin is supported by blockchain technology, which is in the current world…is impossible to hack!! Bitcoins are created digitally through a “mining” process that requires powerful computers to solve complex algorithms and crunch numbers. Currently, Bitcoin is created at the rate of 25 Bitcoins every 10 minutes and will be capped at 21 million, a level that is expected to be reached in 2140.

On the other hand, Fiat money is a centralized currency which is governed by the central authority (central banks) and can be manipulated by the government as and when needed by them. The classic example is the currency devaluation of Yuan exercised by China to boost its exports. Fiat currency issuance is a highly centralized activity. While the bank regulates the amount of currency issued under its monetary policy objectives, there is theoretically no upper limit to the amount of such currency issuance. The classic example to the same right now is the world’s most accepted currency- the US Dollar, wherein the Fed is creating trillions of dollars as we speak to fight the current COVID-19 pandemic just to keep the financial system from collapsing. The aftermath of excess money printing can be known from what happened to Zimbabwe and Venezuela.

Adding to the current fiat money market, Investment strategist and Author Jared Dillian said “The dollar has no real intrinsic value, backed only by the full faith and credit of the US government” explaining further he says: Under a fiat currency system, the government says that a dollar is a dollar. Its value relative to things such as other currencies and gold is determined on global market….if there are too many dollars in circulation, the monetarists would say that the value of those dollars has diminished, eventually leading to higher prices for things.

In other words, money is losing its meaning!!

Are there any drawbacks of Cryptocurrency?

Just like a coin has two sides, cryptocurrency also has its own drawbacks, because of the anonymity and untraceable nature of cryptocurrency, it attracts illegal activities including money laundering, drug peddling, smuggling and weapons procurement. This has attracted the attention of powerful regulatory and other government agencies such as the Financial Crimes Enforcement Network (FinCEN), the SEC, and even the FBI and Department of Homeland Security (DHS). Though new security means are under development by data experts to overcome this challenge.

Why Bitcoin?

When we think of Cryptocurrencies the first thing that hits our mind is Bitcoin, of course there are Altcoins (Alternative of bitcoins) like litecoin, Monero, Dogecoin, Petro, etc. But Bitcoin is the only prominent and relatively stable and mature virtual currency in terms of value in the market right now. The easy availability and its generation by the mining process is easy to learn and exercise as well. You can even say that it is the bias of human nature to be attracted to Bitcoin after all the wonders miners and investors have seen during its rapid price surge in 2017.

Benefits of Bitcoin:

Payment independence

Low fees & fast transaction

Transparency

Counterfeit-proof

Decentralized

Security & control

Currently, Bitcoin is the most expensive cryptocurrency in the market followed by Maker, Bitcoin Cash, Bitcoin SV and Ethereum.

Why are you talking about it just know?

Simply because “Bitcoin is immune to coronavirus!” The world was already on brink of an economic crisis and the current coronavirus outbreak was just an extra fuel to a much larger economic recession. Economies all over the world are affected by the same, manufacturing and supply chain is severely hit. This ultimately affects the value of the stocks market, commodities market and obviously the currencies market because of the halt on import and export of goods and services. Moreover, in times where market turmoil, digital money and fintech apps have seen usage growth significantly. In fact, the COVID-19 pandemic has fuelled a 72% surge in the use of fintech apps in Europe during the last few weeks as people globally try adapting to new working conditions. Digital money is safe-to-use to provide remote payments – a quality one merely thought of as mostly just a convenience before, but now the most important thing that the world prefers is electronic payments to the risk of handling potentially virus-infected physical currency. Not only this, the decentralized nature of Bitcoin makes it more useable and preferred mode for transactions. Bitcoin is an asset that has almost unlimited potential in terms of price growth, and as Pantera Capital’s estimates show, new price records can be expected in 2021. As the world progresses and fights back against the pandemic, Bitcoin’s value and acceptance shall grow, from routine payments to much more sophisticated uses yet to be imagined and created by necessity being the mother of invention. Amid the current crashing global markets a new idea of shifting towards buying non-stock assets like cryptocurrency is gaining a lot of popularity.

Robert Kiyosaki, author of the best-seller “Rich Dad, Poor Dad” argued that the coronavirus pandemic is great for Bitcoin and Bitcoin ultimately stands to go parabolic after the coronavirus ends. He is so positive about Bitcoin that he called it People’s Money.

Tim Draper, an American venture capital investor says that he is certain that the lockdown and money printing initiated by world governments is going to make fiat less worthy and could push people to Bitcoin. He urged on saying that Bitcoin could be a key player in helping to recover from the economic meltdown after the pandemic gets over.

Nassim Taleb, author of the best-seller “The Black Swan” has urged Lebanese citizens to turn to cryptocurrencies, after the Bank of Lebanon increasingly impose tighter controls amid a deepening financial crisis.

Has it already started showing its magic?

Well, let’s just say it has started and the actual potential of Bitcoin is yet to be seen. Some of the points that might help you understand the actual picture of Bitcoin or Cryptocurrency during this pandemic is as follow:

The active Bitcoin supply within the last 2-3 years has reached a new all-time high of 2,774,058.

While the spot market collapsed, Bitcoin futures market saw high turnover, the aggregate daily volumes reached an all-time high of $37.24 billion on 12th March.

Binance, the world’s largest cryptocurrency exchange by market volume recorded the highest ever quarterly volume as evident/analyzed from its profits burning report.

Coinbase, a secure platform for trading cryptocurrencies saw a massive trading volume during the last week of March of around $2 billion in just two days.

Digital Asset Management company Grayscale revealed cryptocurrency demand is on the rise as it reported it’s highest-ever $503.7 million inflow in Q1 2020.

Russia has increasingly engaged into crypto services amid the current coronavirus outbreak. Traffic on Crypto exchange has surged by 5.56% within a month.

Bitcoin exchanges in India are resuming direct bank account deposits & withdrawals using Indian rupee following the Supreme Court’s crypto ban reversal. South Korea approved the trading of cryptocurrencies in the country.

Millions of Americans received their $1200 stimulus checks amid COVID-19 from the government and Coinbase’s $1200 orders of crypto exponentially increased from the US itself.

China tests Digital Yuan. A pilot version of a wallet app for China’s digital yuan is available for download in 4 cities for initial trial.

Italy has endorsed crypto adoption and the COVID-19 outbreak has urged Italian bank, Banco Sella to launch a Bitcoin trading service via bank’s hype platform. The Italian Red Cross deployed a tent bought with Bitcoin donation!!

Binance has enabled its users to buy and sell crypto with Bolivars, the national fiat currency of Venezuela. The daily Bitcoin trading volume of Venezuelan P2P exchange LocalBitcoins is rising from February.

The Reserve Bank of Zimbabwe is developing a regulatory sandbox for cryptocurrency companies to boost the crypto usage in the country.

Just an observation note that the last two-point talks about those counties which have faced severe consequences of hyperinflation, one of the key factor driving it was excess printing of money (Fiat money). And now they are trying to fix this using a decentralized virtual currency with a new ray of hope. The third last point talks about one of the worst coronavirus hit country, and even they are taking a stand to fight against it using the cryptocurrency (Bitcoin).

So in my view, I think this downside of coronavirus outbreak is going to be positive for Bitcoin as well as other cryptocurrencies in an urge to become financially independent, a hope for many severely affected countries and by investors as a potential income source.

Disclaimer: The opinions expressed in this article are those of the author. They do not reflect the opinions or views of Krea University or its members.

The blog is written by Parijat Roy. The Author is a MBA student of IFMR GSB at Krea University.

Food security means all people at all times, must have access to the basic food they need.

According to Food and Agriculture Organization of the United Nations (FAO), currently, around 820 million people around the world are suffering from chronic hunger and approx. 113 million are suffering from acute and severe insecurity i.e. hunger so insecure that it can pose a threat to their lives and livelihoods. Which are the groups more vulnerable to food insecurity? Vulnerable groups include the farmers, fisherman and pastorals who are hindered from working at their land and livestock amid the lockdown imposed due to COVID-19. They are facing challenges to sell their products or buy essential inputs due to income losses. Another group hit hardly by the pandemic are the children relying on free mid-day meals offered at govt. schools. Closure of all educational institutions have led millions of children suffer from hunger due to lack of daily meals and no formal access to social protection. This can pave the way for malnutrition which at present, accounts for 10.8% of the global population. Informal workers are also hit by massive job losses and food insecurity. In India, as per the latest Economic survey, 93% of the total workforce are informal workers.

Are the global food supply chains at risk? As per the predictions of FAO, the global cereal stocks are going to remain at sufficient levels for the year 2020. But there are negative implications for fisheries and aquaculture. Logistics issues such as restrictions in transportation, border closures and reduction in demand by restaurants and hotels will create market changes, thus affecting prices. Shortage of labour shall also create hindrances in food supply. In India, this is the peak season wherein crops like wheat, gram, lentil, mustard etc are harvested. Migration of laborers amid the lockdown will cause panic in the supply chain of such crops. Kazakhstan, for example, one of the largest producers of wheat flour has banned its exports along with others such as carrots, sugar and potatoes. Many of the ASEAN countries like Indonesia, Vietnam, Cambodia are facing fall in supply and rise in prices of staple food items such as sugar, salt, rice, onions etc.

Hence amid nationwide lockdown declared by several countries, the implications on food supply leading from shortage of labour, must be taken care of. India has been following a price-support based policy called Minimum Support Price (MSP) which at the current scenario is extremely crucial to fight any food crisis. India announced a ₹1.7 lakh crore ($22.6 billion) package contributing to food security for the vulnerable sections by providing 5 kg wheat/rice for each person free of cost for 3 months. However, the coverage of such distribution system is low in urban areas which is about 50% as per a survey done by International Food Policy Research Institute, as a result of which many urban poor might be left out. The extra grains pumped into the supply chain might depress prices in the long run, affecting small farmers and businesses. Hence all such relief packages introduced by various nations are just a beginning. Government needs to effectively plan how much and for what length of time the food system can supply the social safety net. Further, international cooperation and smooth functioning of global trade is necessary. As rise in food prices are highly likely, developing countries such as Laos or Myanmar, depending on imported food are highly vulnerable to food crisis. Hence, countries must review their taxation and trade policies for ensuring a favourable environment in global food supply.

The blog is written by Amit Agrawal. The Author is a MBA student of IFMR GSB at Krea University.

The Era of the Fourth Wave?

Total worldwide debt had never been higher. And yet, there’s a little sign of this current wave retreating any time soon. Now with the Coronavirus outbreak being declared a pandemic, governments have announced hundreds of billions of dollars in stimulus packages that will send debt even higher. So, how worrisome is the situation currently?

Global borrowing is growing rapidly so much so countries fear that it might be on the verge of unsustainability. The Institute of International Finance estimates total worldwide debt (which includes borrowings from households, companies, and government) surpassed $253T at the end of September 2019. It is more than thrice the global GDP, 2018 ($84T). This accounts for a $32,500 debt per person for 7.7 billion people. IIF worries more as it is only going to increase.

The World Bank believes the speed and scale of this debt wave is something we should all be worried about. It has asked all governments to make it a primary concern.

Talking in lay man’s terms, debt is created when one party borrows from another to buy something, they wouldn’t normally be able to buy. The interest rate plays a crucial role here. At present, interest rates around the world have fallen to historically low levels. This has made it cheap to borrow from banks.

Recently, the United States (The Fed, led by Chair Jerome Powell) slashed the interest rates to zero as part of wide-ranging emergency intervention. Fed would be buying at least $700 billion in government and mortgage-related bonds as a part of a wide-ranging emergency action to protect the economy from the impact of coronavirus. The move, the most dramatic by the US central bank since the 2008 financial crisis, is aimed to keep financial markets stable thus making borrowing costs as low as possible due to business shutting down globally and the US economy hurtles toward recession.

In addition to rate cuts, the Fed announced that it is restarting the crisis-era program of bond purchases known as “Quantitative Easing”, in which the central bank buys hundreds of billions of dollars in bonds to further push down rates and keep markets flowing freely.

The Fed’s action to inject a large $1.5 trillion into the bond market ensures sufficient liquidity.

Trump has urged the Fed to make the nation’s interest rates negative, something that has never happened before in the United States. Powell said it was unlikely he would make U.S. rates negative. Negative rates work by effectively paying borrowers to take out loans and requiring people and businesses that deposit money to pay a fee rather than earn interest (Source: The Washington Post on March 16, 2020).

But what actually happens when the interest rate plunges in the economy?

The Federal Open Market Committee (FOMC) of the Federal Reserve meets regularly to decide what to do with short term interest rates. When the Fed “cuts rates”, this refers to a decision by the FOMC to reduce the federal fund’s target rate (Source: investopedia.com). The target rate is a guideline for the actual rate that banks charge each other on overnight reserve loans. Rates on interbank loans are negotiated by the individual banks and usually stay close to the target rate.

The Fed lowers the interest rates in order to stimulate economic growth. Lower financing costs can encourage borrowing and investing. However, when rates are too low, they can spur excessive growth and perhaps inflation. Inflation eats away at purchasing power and could undermine the sustainability of the desired economic expansion.

[Financing] A rate cut could help consumers save money by reducing interest payments on certain types of financing that are linked to prime or other rates, which tend to move in tandem with the Fed’s target rate.

[Mortgages] A rate cut can prove beneficial with home financing, but the impact depends on the type of mortgage the consumer has (fixed or adjustable). For Fixed-rate mortgages, a rate cut will have no impact on the monthly payment amount. A Fed rate cut changes the short-term lending rate, but most fixed-rate mortgages are based on long-term rates, which do not fluctuate as much as short-term.

The link between inflation and mortgage rate is direct. Inflation is an economic term describing the loss of purchasing power. When inflation is present within an economy, more of the same currency is required to purchase the same number of goods. More money is required to purchase the same amount of item(s) because each dollar holds less value. Meanwhile, mortgage rates are based on the price of mortgage-backed securities (MBS) and mortgage-backed securities are U.S. dollar-denominated. This means that a devaluation in the U.S. dollar will result in the devaluation of U.S. mortgage-backed securities as well. When inflation is present in the economy, then, the value of a mortgage bond drops, which leads to higher mortgage rates.

This is why the Fed’s comments on inflation are closely watched by Wall Street. The more inflationary pressures the Fed fingers in the economy, the more likely it is that mortgage rates will rise.

[Savings Account] Consumers usually earn less interest on their savings due to interest rate cuts. Banks will typically lower rates paid on cash held in bank certificates of deposits (CDs), money market accounts, and regular savings accounts.

[Sovereign Debt] Governments take on debt which they can use to stimulate the economy by funding infrastructure. It becomes a matter of concern if any of the debts become excessive.

Loans to countries with developed economies, like Canada, Denmark or Singapore, are generally seen as safe investments. That’s because even if governments spend beyond their means, lawmakers can raise taxes or print more money to ensure they pay back what they owe. But loans to governments in emerging markets are generally seen much riskier which is why these countries will sometimes issue debt in a foreign, more stable currency. Although this allows them to attract more investors from abroad looking for bigger returns, an economic slump, weak domestic currency or high debt burden can make it difficult for governments to pay them back.

The most important risk, that comes to national borrowing, is countries not able to pay debt obligations and default. For example, the Russian Financial Crisis in 1998, the Argentinian Crisis in 2001, and recent Lebanon in 2020. Over the last 50 years, there have been four waves of debt accumulation – 1970-89, 1990-2001, 2002-09, and 2010-present. We are currently in the midst of the fourth wave.

In the first wave, many Latin American and Caribbean countries (LAC) began to borrow extensive amounts of money from US commercial banks and other creditors to support development. There wasn’t any problem faced by both parties. Interest rates were low and Latin American economies were flourishing. But in the background, the debt wave was rising. At the end of 1970, the region’s total outstanding debt reached a height of $29 billion. By the end of 1978, that number had shot up to $159 billion. Four years later, it had more than doubled to $327B (Source: Federal Deposit Insurance Corporation, 1997). In the 80s, major economies began hiking up their interest rates as they baffled inflation. Oil prices were sliding, and the world economy was entering a recession. In 1982, the starting gun of Latin American debt crisis was effectively fired, when Mexico announced it would not be able to service its debts. This move quickly sparked a meltdown across the region, with a fallout spreading to dozens of emerging economies worldwide. The debt crisis of 1982 marked the end of the Import Substitution Model (ISM) (Source: scielo.br). In 1983 Mexico, like other Latin American countries, started the transition to a Neoliberal Model (NM), a model of an open economy, facing outward, characterized by the conversion of manufactured exports into the axis of accumulation pattern. Many Latin American countries were forced to devalue their currencies to keep exporting industries competitive in the face of a sharp economic downturn (Source: World Bank, 2020). Between 1981 and 1983, Argentine Peso weakened against the US $ by 40%, Mexican Peso by 33%, and Brazilian Real by 20%. (Source: World Bank, 2020). Overall 27 countries rescheduled their debts; out of which 16 were in Latin America (Source: Federal Deposit Insurance Corporation, 1997).

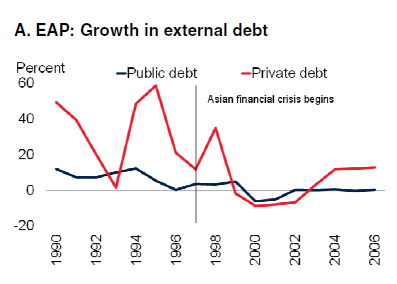

The second wave ran from 1990 to 2001 – It was unlike the first wave, here, debts in the private sector played a pivotal role. As we know, in the late 80s and early 90s, many advanced economies deregulated their financial markets. The policy changes made way for the consolidation of banks due to which these bigger bank operations became increasingly global. This helped prompt a massive surge of capital into emerging markets, with falling interest rates and a slowdown in advanced economies also fueling the surge. Developing economies on the other hand started to withhold a lot of debt, especially Malaysia, Indonesia, South Korea, the Philippines and Thailand.

Yet the growing wave of debt went largely unnoticed, as the debt was growing rapidly but so was GDP. This means the ratio between the two remained consistent. And from the graph we see that most of the debt remained latent in the private sector.

A currency crisis in Mexico in 1994 thrust international investors back into panic-mode, with a country’s default a decade earlier was not being a good relief. Yet, while a $50 billion bailout from the US and the IMF meant that Mexico was narrowly able to avoid a default this time. But it wasn’t able to stop ‘defaults’ lurking at the doors of other countries. It led to abrupt stop and reversal of capital flows in 1997. By this time Malaysia, Indonesia, South Korea, the Philippines and Thailand had developed a dependence on borrowing. Coupled with several other policy failings, this surged into a crisis in East Asia’s financial sector leading to another global downturn. While other countries recovered from the Asian Financial Crisis, international borrowing followed at a brisk pace.

We now enter into the Third Wave which lasted from 2002 to 2009. At the end of the previous century, the US removed barriers between commercial and investment banks, while the European Union (EU) encouraged cross-border connections between lenders. This paved a way for the formation of so-called “megabanks”. These banks led to a sharp increase in private sector borrowing, particularly in Europe and Central Asia (ECA). Defaults in the US subprime mortgage system piled more and more pressure in the country’s financial system, pushing it to the brink of collapse in the second half of 2007 and 2008. The shockwave reverberated across the world, with one economy after another falling into a deep, albeit short-lived (Source: cnbc.com), recession. In 2009, the US recession hit its lowest level of economy since the Great Depression. The World Bank, in its latest edition of ‘Global Waves of Debt: Causes and Consequences’, says that we’re currently in the midst of the fourth wave of Global Debt. So in order to learn from the last three crises and avoid debt, governments must maintain a debt management system and transparency a top priority. This wave had seemed to cover all emerging markets and developing economies (EMDEs). It follows the same characteristics of the previous three including prolonged periods of low-interest rates and changing financial landscapes which encourage more borrowing.

But the World Bank has called the current wave as “the largest, fastest and most broad-based” of them all. It includes concurrent build-up of public and private debts, involves new types of creditors and is much more global.

With the Arab Spring uprising from 2010 in Egypt and previous encounters in other parts of the Middle East led to a significant drop in economies of the Middle East further fueled by political instability. Five years after the Arab Spring uprisings began (2015), Egypt, Jordan, Morocco, and Tunisia have achieved reasonable levels of political stability. Yet economic growth remains tepid, and the International Monetary Fund does not expect the pace of expansion to exceed 1.5% per capita this year (Source: imf.org, Articles 2015). Despite significant progress in building stable governments, these countries remain subject to political risks that scare private investors. But private investment was modest before the uprisings of 2011, when such risks were already high (Source: weforum.org).

However, as the Coronavirus pandemic threatens to sink the world economy, the moment of stemming the tide may have passed.

GLOBALISATION AND DEBT CRISIS

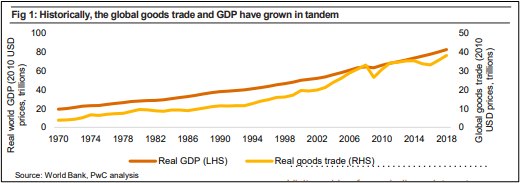

A defining feature of the global economy since at least the 1970s has been globalisation—the bringing together of economies predominantly via more liberal trade flows (Source: pwc.com). The global volume of merchandise traded slowed down dramatically and even went in reverse in 2019 in contrast to a 21st-century average growth rate of about 3.4% per annum (Source: CPB World Trade Monitor). In his 1989 essay, ‘The End of History?’, political thinker Francis Fukuyama famously predicted the triumph of liberalism, which became a catalyst for globalisation and the associated liberalization of the economy. The fall of the Soviet Union, which many happily attributed to as the fall of the socialist order, and the downfall of states that leaned towards the left spectrum of ideologies, gave way to internal tumult — signaling that the juggernaut of neoliberalism was unstoppable (source: thehindubusinessline.com). The new model was a consequence of global trends to shift production systems overseas as a result of the “great crisis” started in the late 1960s in the major developed countries, following the end of the long boom of the post-world war period. Globalization became a strategy to “step out” of the crisis for the most powerful and internationalized banks. In turn, indebted countries, large domestic private groups, corporations and banks operating within it, as well as governments, found in globalization an option to convert their businesses and focus them on the foreign market, in the Mexican case mainly the United States.

This graph shows that growth in merchandise trade flows and the global economy have been intrinsically linked. In our main scenario for 2020, we expect the global economy to expand at a rate of around 3.2% in purchasing power parity (PPP) terms which is below the 21st century average of 3.8% per annum. In our main scenario, we expect all of the major economies to grow by accommodative financial conditions. US economic activity is likely to expand by around 2%, in line with its potential rate.

But countries are going to be extremely wary of the superpower that China will become and would like to disengage. Stimulus packages — be it in the US, France, Germany — have an overwhelming emphasis on small businesses, which really were at the heart of their post-war industrialization strategy, and one will see industrial policy whose flip side will be import substitution. So, globalisation will be defined in a very different way. Once you talk of import substitution, you focus more on your domestic skills. The movement of personnel will follow the formula of economic needs, so the U.S. may keep importing skilled personnel from India (Source: thehindu.com/opinion).

Countries will reconfigure their economies to look at import substitution with greater clarity now, as the perils and pitfalls of overdependence on foreign supplies become clear. Import substitution, that had become a bad word, maybe back in currency.

‘Festina lente’: More haste, less speed

The Slow Food Movement which started in the 1980s to refrain people from eating fast food, slowly turned towards affecting Globalisation. To a world addicted to ever greater connection speeds, ever faster modes of transportation, and ever more caffeinated feats of multitasking, the go-slowers recommend a perverse resistance to the frenzied scherzo of modern life in favour of a more comfortable adagio (Source: business-standard.com). In the year 2018, The Economist identified several key factors of what it calls “slowbalisation”. The portion of trade as part of the global GDP has fallen. Multinationals have seen a drop in their share of global profits. FDI tumbled from 3.5 percent of global GDP in 2007 to 1.3 percent in 2018. The US-China Trade War further fuels the entire breakdown. Other reasons that pop up here are the falling costs of moving goods. This directly impacts the services as it is harder to sell services across borders. But this slowbalisation affects positively, as claimed by the Business Standard, as it reduces global carbon footprint, shrinks economic inequality, and reorient national economies toward local growth. The world today faces a number of crises. And that’s why ancients were right when they coined ‘Festina Lente’: more haste, less speed.

Economic globalisation has been a part of the world system since the Silk Road and even earlier. But the modern version dates to the late 19th and early 20th centuries, when railroads, telegraphs, modern factory production, and mass migration converged to create a new worldwide web of connections. As a result of global network, trade increased exponentially until 1914. The outbreak of WWI stopped globalisation at its tracks. It is now fine to claim that it was only after the first World War international NGOs were being able to establish. But this too did not last long. It was only after WWII did another attempt of rebuilding the international community began with the creation of the United Nations and a set of international financial institutions.

Slowbalisation will be meaner and less trouble than its predecessor. It is evident from the fact that globalisation, though it made the world a better place for everyone, too little was done to mitigate its costs. Acknowledging costs and benefits of Globalisation is not enough. We must pay attention to uneven distribution of those costs and benefits. The challenge is now to preserve the political internationalism necessary to address global problems and retrofit global economy to meet the needs of the people and the planet.

The fear and panic triggered by the virus has wreaked havoc in global financial markets. FT says there is a potential warning signal of global recession. The newspaper’s editorial is, interestingly, titled “Coronavirus has put globalisation into reverse…The spread of the epidemic amounts to an experiment in deglobalisation.”The global public response towards the coronavirus pandemic reaffirms such concerns. COVID-19 has given rise to four crucial learnings. The first is the failure of private capital and privatized medical care in ensuring proper healthcare for the public at large. Second, companies cannot take comfort in the fact that poverty, unhygienic conditions or precarious health infrastructure in one remote country is none of their business. This is the globalisation of responsibility, and not globalisation for the sake of profits alone. The third factor is that socialist regimes are better positioned to respond to emergencies. The fourth and most crucial insight is that public problems require public solutions. By default, neoliberalism simply cannot offer answers. The future, especially considering the collapse of globalisation, lies in ensuring a world order where resources are distributed in a much more egalitarian way and are controlled by the public.

With the onset of the quarantine lockdowns and curfews as solutions against the pandemic, there has been a talk about the world pushing toward the gig economy. Nagesh Kumar, Director, UN Economic and Social Commission for Asia and the Pacific (UNESCAP) said in an interview with The Hindu, “The first priority of every government would be to create jobs for its own people. In a high unemployment scenario, hiring ex-pats won’t be in favor. In any case, there had been rising protectionism on this front already.” Gig economy foresees the traditional economy of full-time workers who rarely change positions and instead focus on a lifetime career. The people we see around are mostly willing to work part-time or in temporary positions, not because of their inability to crack highly paid jobs but due to overpopulated competition within a handful of sectors. Youngsters find themselves at ease and are often dependent on these gigs (Ola, Uber) as their primary source of income and bereft of any access to any form of health insurance or social security cover. They can therefore scarcely consider taking time off work for any reason. This precariousness could now pose a massive threat to the public interest as these workers tend to interact with dozens of people a day and could become the new “super-spreaders” of the coronavirus. Workers at the frontline must, therefore, be provisioned accordingly to make them more resilient, and also provided with a safety net robust enough to enable them to take time off work if they feel symptomatic or support them in the event of a total lockdown.

Finally, the gravity of this crisis demands a change in individual behavior and social norms at their core. Only a change in individual behavior can eventually lead to the world overcoming this crisis. We must fortify our communities even as we practice physical isolation. One person’s precariousness is now society’s problem.